Information is vital to a business leader’s ability to make decisions, and when it comes to financial information, cost accounting plays a key role in ensuring decisions are fully informed. Understanding costs at an organization can be complex, as some are fixed and others are variable, and many steps in organizational process incur costs.

What is Cost Accounting?

The cost accounting definition distinguishes it from financial accounting, which reports to external financial statement users. Cost accounting is an internal tool for business managers. Because this discipline is an internal resource, cost accounting standards can be more flexible to support business needs and aren’t bound by rigid regulations.

Organizations use cost accounting to identify variable and fixed costs in a production process, which enables leaders to measure financial performance and informs their business decisions.

Types of Costs

Cost accounting includes four main types of cost:

- Fixed Costs

These costs can’t be adjusted based on production levels. They can include mortgage or lease payments for the office building or business equipment that costs a monthly rate.

- Variable Costs

These costs are directly related to production levels, when the business must purchase more raw materials or supplies to prepare for an uptick in production. For example, a grocery store might have a surplus of supply purchasing to prepare for Thanksgiving shoppers.

- Operating Costs

These costs are part of the business’ daily operations, like rent and utilities, and they may be fixed (rent) or variable (utilities).

- Direct Costs

These costs are directly related to creating the product. For example, if a florist spends three hours producing arrangements for an event, the direct costs include the flowers required and the labor hours for the florist.

Indirect costs, though also part of an organization’s total costs, cannot be directly related to a product, because of imprecise measurements or challenges associating these costs with specific products. For example, the cost of electricity can be an indirect cost as it is difficult to isolate to a single production line.

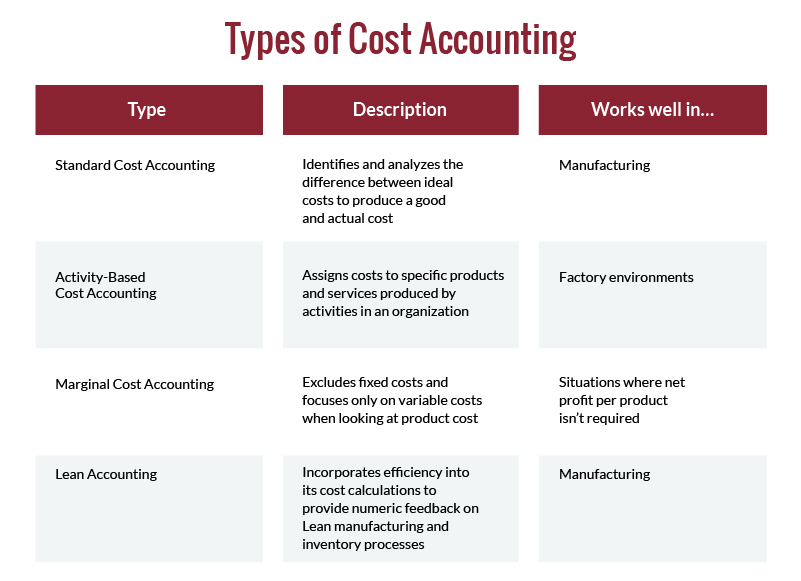

Types of Cost Accounting

Within the discipline of cost accounting, there are four major types of cost accounting:

- Standard Cost Accounting

Identifies and analyzes the difference between ideal costs to produce a good and actual cost to do so. This is often used by manufacturers to understand the costs that should have occurred based on previous production or market research. The standard costs include the product cost, material cost, labor cost and overhead costs. With this information, managers can plan and budget, projecting an expecting net earnings assuming standard production costs.

- Activity-Based Cost Accounting

Assigns costs to specific activities in a production process, and is often leveraged in factories. These activity costs are then broken down again by products and services based on the product’s actual resource use. This typically follows several steps:

-

-

- Identify activities, which may include purchasing materials, processing them and transporting them.

- Identify expenses within each activity. These costs, known as a cost pool, represent the total cost for that activity, but are often may unique costs. For example, within transportation, costs might include fleet rental, fuel, and the costs to pay drivers.

- Identify the cost drivers. A cost driver is a cost within the activity that has the power to change (drive) the costs. Often, this is the human capital cost of paying employees. In transportation, this might be the size of the transportation vehicles as well.

- Understand the rate of each activity (divide total cost by number of cost driver units), and calculate the total costs.

-

- Marginal Cost Accounting

Excludes fixed costs and focuses only on variable costs when assessing product costs. Fixed costs, like rent or electricity, are included in the Income Statement as expenses, but not associated with a specific product. Instead, the marginal cost of the product is only its variable costs, which includes labor and materials costs. When production increases, so do variable costs. Net profit at a product level can’t be calculated, because the fixed cost isn’t allocated to individual products, but the differences between the total revenue and the total variable costs is calculated.

- Lean Accounting

Incorporates efficiency into its cost calculations to provide numeric feedback on lean manufacturing and inventory processes by assessing the time order processing takes overall, and considering the cost to hold on to excess inventory, which include opportunity cost and holding costs, rather than simply counting inventory as an asset.

Cost Accounting vs. Financial Accounting

A key focus for cost accounting is providing timely information that helps managers achieve their organization’s goals. To achieve this, cost accountants must:

- Measure, analyze and report financial and nonfinancial information

- Provide support for managerial decisions

- Assess the costs of the individual components of a product for sale

- Recommend an approach to allocate overhead costs for products or departments

- Provide information and guidance around whether the business should accept an order at a special price

On the other hand, financial accounting is external, presenting the company’s financial statements to investors or creditors, including revenues, expenses, liabilities, and assets.

Cost accounting’s internal focus means cost accounting is not held to standards like the generally accepted accounting principles (GAAP) and can vary based on management’s needs to inform budgets, establish better cost control, or improve company margins.

Cost Accounting: A Part of Florida Tech’s Accounting Curriculum

Cost accounting is one of many in-depth courses that comprise the curriculum of Florida Tech’s online accounting degree programs. Explore Florida Tech’s BA in Accounting program to learn more.